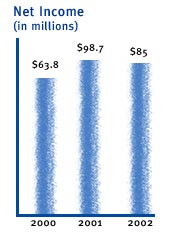

CareFirst reported net income of $85 million for 2002, down nearly

14 percent from the $98.7 million reported in 2001. The decrease

was due primarily to an “other than temporary impairment”

(OTTI) adjustment in the company’s investment portfolio. Excluding

this OTTI adjustment and adjustments for discontinued operations,

net income for 2002 was approximately $105 million, an increase

of about 13 percent over the prior year.

Membership grew 4 percent in 2002, reaching 3.24 million members

by year-end. Enrollment growth was particularly strong in Delaware

where the addition of several large accounts increased total membership

by 16 percent. Total enrollment at the Delaware affiliate has increased

49 percent since the affiliation with CareFirst. Membership growth

in the Washington area was also strong in 2002 – up nearly

12 percent.

CareFirst’s market strength rests on its ability to effectively

contain administrative expenses, to maximize its brand identity

and to maintain the company’s high standards of customer service.

CareFirst administrative cost ratio in 2002 dropped to 8.4 percent

of total revenues, down from 9.1 percent in the prior year. For

CareFirst customers, this means that approximately 90 cents of every

revenue dollar last year was allocated to health care and related

services.

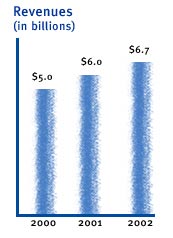

CareFirst’s revenues on consolidated operations, including

premiums and premium-equivalents, rose to $6.7 billion in 2002,

up from slightly less than $6 billion in 2001. The company’s

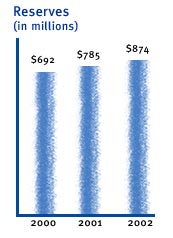

reserves – a measure of financial strength used to assess

an insurer’s ability to cover claims, meet unexpected contingencies

and provide a source of funding to invest in product and service

improvements – rose to $874 million at year-end 2002, an 11

percent gain from year-end 2001, using generally accepted accounting

practices.